Unpacking the numbers on the impact of the ‘Triple Lock Plus’

Since the reveal of a new Conservative pension policy dubbed ‘Triple Lock Plus’, differing figures—from £100 up to £2,000—have been circulating about how much money pensioners could save.

Under the Conservatives’ proposal the personal tax free allowance (the amount you can earn before paying income tax) would increase solely for pensioners to match the rate pensions will also rise annually, at a reported cost of £2.4 billion a year.

As part of the existing ‘triple lock’, the state pension increases each year in line with either average earnings, inflation or by 2.5%—whichever is the highest.

The standard personal allowance is currently £12,570 per year and the full new state pension is now £11,502, while the basic state pension is £8,814 (which one you get depends on when you were born). These rose by 8.5% in April, following a 10.1% rise the previous year.

Similar increases to the full state pension in line with those seen in 2023 and 2024 could see it exceed the tax-free personal allowance limit within the next two years. And many pensioners—62% in 2022/23—already pay income tax.

Join 72,547 people who trust us to check the facts

Subscribe to get weekly updates on politics, immigration, health and more.

What would the financial impact of the ‘plus’ be?

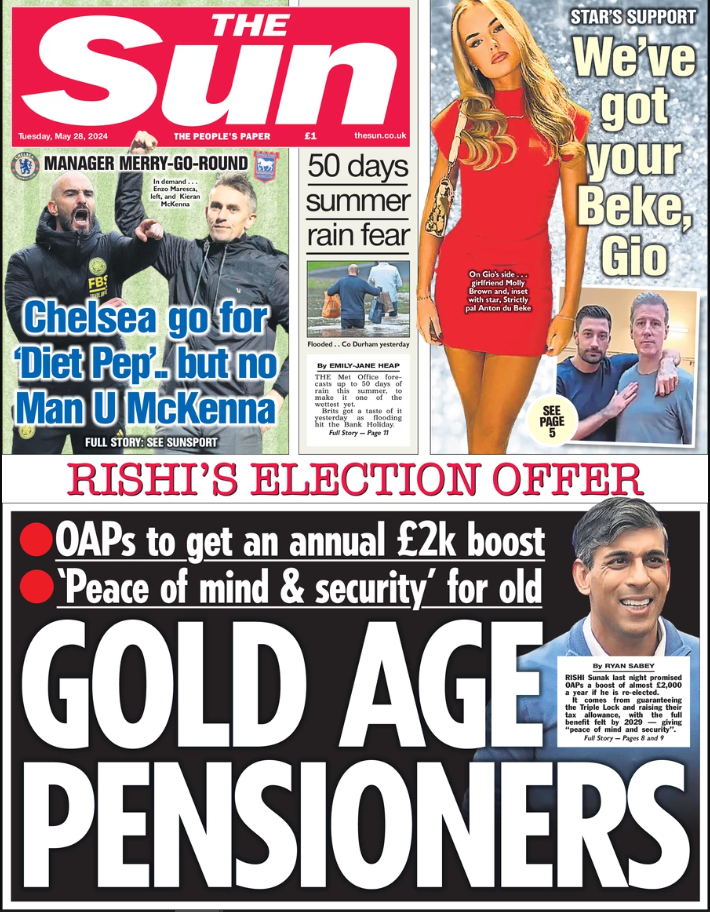

The Sun reported on its front page on 28 May that Rishi Sunak has promised pensioners a figure of “almost £2,000 a year” by 2029 if re-elected.

{kind=link}

Other media reports cite yearly savings ranging from an initial £100, up to £275 or £300.

These figures are all looking at slightly different calculations and timeframes. The £100 to £300 figures refer to the amount pensioners would reportedly save in tax they would have otherwise had to pay if the personal allowance wasn’t increased in line with pensions.

In their news release on their new pension ‘plus’ policy, the Conservatives reportedly said eight million people claiming the state pension would receive a tax cut worth £100 next year in this way, which would increase as the ‘age-related’ tax free allowance grows, up to nearly £300 a year by the end of the parliament.

But Institute for Fiscal Studies Director (IFS) Paul Johnson posted on X that the “the £100 ‘saving’ next year is mostly just avoiding a £100 tax increase, rather than an actual giveaway”.

The £2,000 figure meanwhile is a combination of both guaranteeing the existing triple lock and the proposed increase in the personal allowance for pensioners (which has been frozen in recent years).

So it’s a combination of an increase in the amount of money pensioners would be set to receive in their pension, and the tax money they would otherwise have had to pay.

However, the £2,000 ‘boost’ from the Conservative party for pensioners needs the context that Labour and the Liberal Democrats have also committed to protecting the triple lock (Labour’s commitment to the triple lock is reported in the full Sun article). The core increase in the state pension will likely go ahead no matter which party forms the next government.

A Conservative advert on X (formerly Twitter) on 28 May claimed that people will be facing “retirement tax bills” and that “Labour will tax your pensions” if they are elected. Labour has criticised the Conservative policy proposal, but says it is committed to the triple lock, under which pensioners' income from the state pension alone may go above the tax threshold in future.

The Sun has also reported Treasury Minister Laura Trott describing Labour’s policy on the triple lock plus as a “retirement tax”.

However, the ‘Triple Lock Plus’ policy needs to be viewed in context with changes to tax thresholds.

What has happened to tax thresholds?

In 2021 when Mr Sunak was chancellor, the government froze the personal allowance and the higher rate threshold for four years, which was then extended by Jeremy Hunt when he was chancellor until 2028, rather than the default policy of increasing it in line with inflation (using the Consumer Price Index).

Analysis by the IFS estimates that the new age-related personal allowance policy would take around 750,000 pensioners (6%) out of income tax by 2030 compared to current government policy, and increase the incomes of around two-thirds of pensioners—7.5 million people.

According to the IFS, when viewed in real, inflation adjusted terms, the current personal allowance for pensioners is around 10% lower than in 2010 (when it was set higher for people over 65 and 75 earning less than £22,900 a year) whereas the allowance for working-age people is now 30% higher.

The Coalition government announced it was phasing out the higher personal allowance policy for people over 65, a move that was dubbed the “granny tax”, in 2012.

You can follow more of our politics coverage during the general election campaign trail on our live blog.

Image courtesy of Christopher Bill