Do train operating companies earn 'massive' profits?

"Train operators invest little cash but take massive profits ... For every pound the railway barons put in, they get £2.47 back."

The Guardian, 4 November 2013

Ever since its privatisation in the 1990s, the UK's rail industry has faced constant scrutiny, and calls persist from some quarters for the service to be taken back into public ownership. Familiar stories of rail fare increases year after year, severe overcrowding on many commuter services, and most recently 'massive' profits for train operators haven't helped the industry's cause.

Rising fares and overcrowded services aren't suprising or difficult to prove. Profits are much less straightforward however, and recent comments in the Guardian need scrutiny of their own.

Join 74,000 newsletter subscribers who trust us to check the facts

Sign up to get weekly updates on politics, immigration, health and more.

Subscribe to weekly email newsletters from Full Fact for updates on politics, immigration, health and more. Our fact checks are free to read but not to produce, so you will also get occasional emails about fundraising and other ways you can help. You can unsubscribe at any time. For more information about how we use your data see our Privacy Policy.

Big returns for train operators?

The nub of the claim as laid out in the Guardian comes from research conducted by the Centre for Research on Socio-Cultural Change (CRESC) at the University of Manchester and the Open University. The Centre's recent research has been highly critical of the inner workings of UK rail franchising, in particular the returns it delivers for Train Operating Companies (TOCs).

Using figures extracted from corporate financial databases, CRESC determined the pre-tax profits of TOCs and compared this with the 'capital' employed by the companies. It's a measure called 'Return on Capital Employed' which is often used to evauate a company's profit relative to the resources they've plugged in to get it.

In other words, a large return on capital means a company has got a great deal of profit out of a little investment. A small return indicates it isn't translating its resources into profits very efficiently. CRESC's analysis suggests that, on average, TOCs get returns of 147% of this measure, by any accounts a 'massive' figure since it means profits before tax are even greater than the capital employed to get it.

However, it's not necessarily the most useful indicator to choose. Train operators work in a highly unusual industry by most accounts: their activities are restricted by franchise agreements which determine which services they must operate and, to an extent, how much revenue they can take away.

TOCs themselves don't tend to own rolling stock (the trains themselves) and the rail infrastructure itself is managed by Network Rail, so resources are being employed elsewhere (Network Rail itself enjoys a modest 1-2% margin on the same measure).

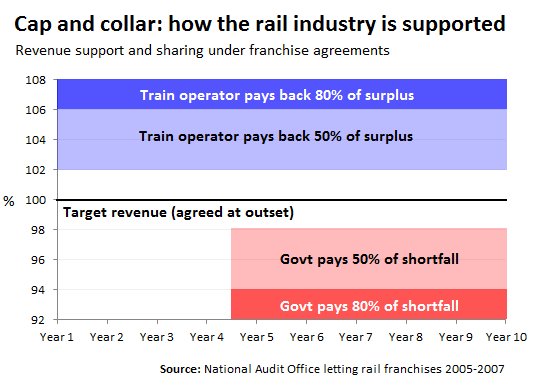

Franchising: taxing success and underwriting failure

All this isn't to say that train operators get very little out of franchising. There is publicly-available data on what TOCs get in and spend their money on, and where the government plays its part.

In 2011-12, TOCs in Great Britain brought in a total of just under £7.9 billion (before subsidy), by far most of which came from passengers (£7.2 billion). Compare that to costs: in the same year TOCs spent £5.9 billion, mainly on staff, rolling stock and charges to Network Rail, leaving a surplus of £2 billion.

But that surplus isn't profit. That's where the government comes in.

When franchises are put out to tender by the government, the bidding companies are often required to set out a 'target revenue' - how much money they expect to bring in from operating the franchise. If they fall substantially below this target (after the 4th year), the government bails them out with support. If they substantially exceed the target, they have to pay back the government, vice versa. It's known as 'cap and collar'.

This process hasn't come without controversy. While train operators argue it forces companies to be competitive in their bidding and that it helped the industry survive the recession, others have criticised the scheme for encouraging reckless revenue forecasts, with TOCs secure in the knowledge they'll be mostly cushioned from their fall. The scheme is now set to be phased out and replaced with one linked to GDP forecasts.

There's obviously a great deal of variation: some TOCs receive millions in support, others pay back as much for the government to reinvest. In 2011/12, Northern Rail drew the most subsidy of £303 million, while South West Trains payed the most back (£243 million).

Profits at the end of the day

Taking these subsidies into account, last year train operating companies enjoyed, between them, a margin of £305 million (3.4%). Analysis from KPMG shows margins similar to this going right back to 1997.

This isn't the same as profit as it doesn't take into account tax deductions during accounting. The House of Commons Library factored these into its own anaysis for the Transport Select Committee. Profits can vary wildly year-on-year, but most companies have a positive balance.

The short answer is that companies vary. Some operate profits and pay premiums to the government, others the opposite.

| Operating profit (£million) | |||

| 2009 | 2010 | 2011 | |

| Arriva Trains Wales | 3.4 | -27.8 | 20.5 |

| C2C Rail | 3.8 | 0.8 | 14.7 |

| Chiltern Railways | 67.5 | 49.4 | -57.1 |

| Cross Country | 3 | -30 | |

| East Coast | 19.9 | 19.3 | 4.6 |

| East Midlands Trains | 16 | 6.6 | -34 |

| First Capital Connect | 30.3 | 37.9 | 2.5 |

| First Great Western | 15.3 | 24.1 | -52.3 |

| First ScotRail | -12.8 | 9.4 | 15.6 |

| London Midland | 22.5 | 30.3 | -2.7 |

| London Overground | 12.5 | 13.3 | 7.5 |

| Merseyrail | -0.3 | -4.7 | 14.9 |

| National Express East Anglia | -8.4 | -12.9 | 29.6 |

| Northern Rail | 3.8 | 9.7 | 35.2 |

| South West Trains | 13.8 | 15.3 | 47.5 |

| Southeastern | 1.3 | 21.8 | |

| Southern | 5.4 | -2 | 18.5 |

| Virgin Trains | -4.3 | -16.4 | 34.3 |

[Companies' figures are for different financial years, so the figures aren't entirely comparable]